WHEN CONFLICT MEETS EXPENSIVE MARKETS

When conflict breaks out in the Middle East, markets usually react in a familiar pattern. Oil rises first, investors become more cautious, and equity markets often weaken. The reason is simple. The region remains central to global energy supply, and when oil prices jump, the effects can spread quickly through fuel, transport, freight and broader business costs. The recent fighting between Iran, Israel and the United States, is a reminder that geopolitical events can affect markets very quickly, particularly when they involve major energy-producing regions.

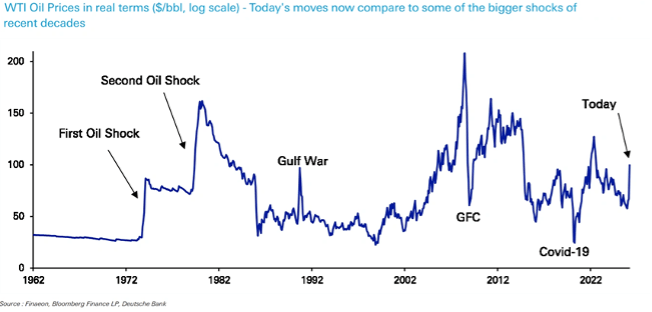

History shows that not every conflict causes lasting market damage. In many cases, the initial market reaction is sharp but short lived. Markets often stabilise once investors gain confidence that the fighting will stay contained and oil supplies will continue to flow. The greatest danger arises when elevated energy prices persist long enough to fuel inflation while dampening economic growth. That was the key lesson from the 1973 oil shock, it also proved true again after the 1979 Iranian revolution, and during the 1990 Gulf War. In those periods, a geopolitical event evolved into broader economic problem.

For investors, it is important to understand that markets do not just react to the conflict itself. They react to what the conflict might do to company profits, inflation, interest rates and household budgets. When oil and gas prices rise, it can push up petrol, transport, manufacturing and energy costs. This places pressure on consumers and businesses, and it can also make it harder for central banks to potentially cut interest rates as quickly as markets might hope.

THE STRAIT OF HORMUZ

This is why the current situation matters. The main issue is not only Iran itself, but the risk to shipping and energy flows through the Strait of Hormuz. It is reported that around one fifth of global oil passes through this route, and that recent developments have pushed Brent crude above US$100 a barrel after a surge of more than 40% in recent weeks. Moves of this magnitude do not only affect petrol prices. They can also lift inflation expectations, weigh on consumer spending and make decision making more complicated for policymakers and central banks.

All of this is occurring against the backdrop of a multi-year rally in equity markets. Entering 2026, valuations were already elevated following a very strong run, with investors still expecting solid gains. When assets are priced aggressively for good news, they tend to become more sensitive to bad news or even small changes in expectations. Conflict can be the catalyst that exposes this vulnerability. Expensive growth shares, cyclical companies, and businesses with high energy or transport costs often come under pressure more quickly than they would in a cheaper market.

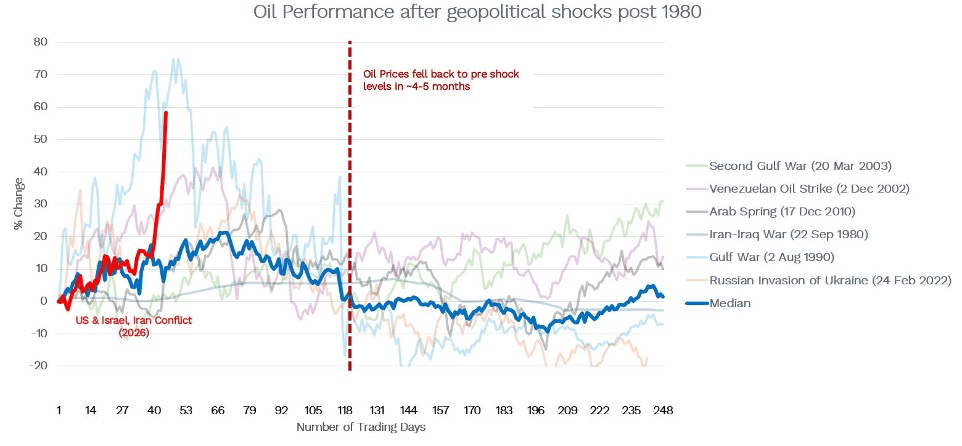

The best-case scenario is a contained conflict and the reopening of shipping routes, which would likely see oil prices ease and investor sentiment recover. A moderate outcome would involve a prolonged period of tension, higher energy prices and greater market volatility, but without a major economic downturn. The worst-case scenario is a broader regional conflict that keeps oil prices elevated for long enough to turn a market shock into a sustained growth and inflation shock. History suggested this is the outcome that ultimately matters most.

Markets can absorb unsettling headlines; they struggle far more when those headlines begin to affect everyday prices and the real economy.

THE KEY LESSON FOR INVESTORS

The key lesson for investors is not to panic in response to every geopolitical shock. Conflicts matter, but their market impact depends on whether they translate into broader economic problems. A well-diversified portfolio is still the best defence. Attempting to move in and out of markets based on breaking news is extremely difficult. For long-term investors, staying calm, staying diversified and focusing on the bigger picture is usually the more effective path.

Importantly, history shows:

- Markets fall before and at the start of wars

- Markets usually recover quickly once uncertainty begins to decline

- Long-term returns remain driven by earnings and economic growth

- Selling during geopolitical panic historically locks in losses.

Written by Chris Lioutas of Genium Investment Services for Mandate Financial Planning CAR Futuro Financial Services Pty Ltd AFSL 238478.

The information contained herein is provided by Genium Investment Consultants Pty Ltd & Genium Investment Research Pty Ltd trading as Genium Investment Services (Genium) AFSL 246580. To the extent that any information provided constitutes financial product advice, it is general advice only. It does not consider the objectives, financial situation or needs of a specific person. Accordingly, before acting on the advice, any person reviewing the information should consider its appropriateness having regard to their objectives, financial situation and needs before making any investment decision. Past performance is not an indication of

future performance. For further relevant information, please see Genium’s Financial Services Guide here.

General Advice Warning: This provides general information and hasn’t taken your circumstances into account. It’s important to consider your particular circumstances before deciding what’s right for you. Although the information is from sources considered reliable, Mandate Financial Planning and Futuro Financial Services Pty Ltd AFSL 238475 do not guarantee that it is accurate or complete. You should not rely upon it and should seek qualified advice before making any investment decision. Except where liability under any statute cannot be excluded, Futuro and Insight do not accept any liability (whether under contract, tort or otherwise) for any resulting loss or damage of the reader or any other person.